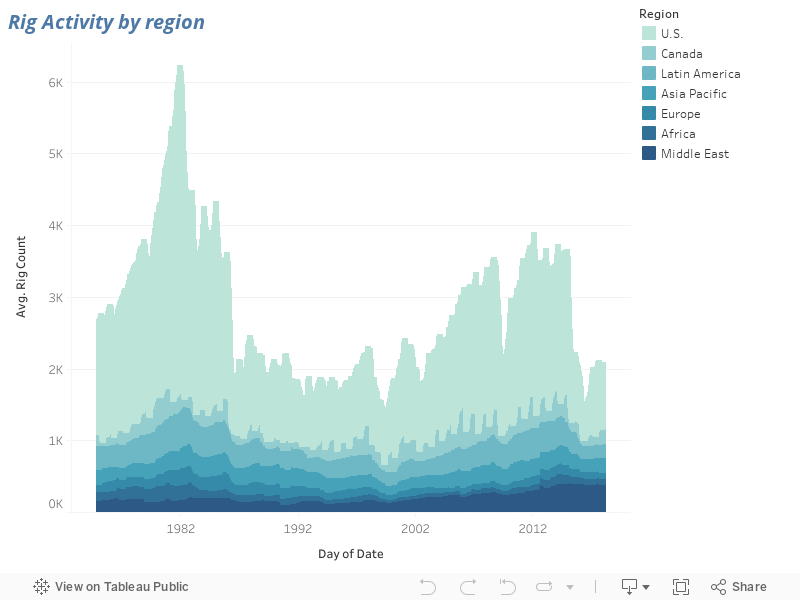

Rig activity throughout the regions of the world changes daily and with it changes the amount of services needed for the oil and gas industry.

Rig counts throughout history and the world varied widely, between 6000 in 1981 and 1100 in 1999. Reasons for wild swings in rig utilization are numerous, among them political, technological, oil demand and oil price, markets.

Technology

The switch from shallow vertical post-holes in fresh basins to higher efficiency horizontal wells in mature basins, and the industry reaching out offshore in deeper water, all led to fewer rigs drilling more productive wells.

As technology advances increase efficiency in mature basins, the make-up of the world active fleet shifts

Oil Price

Oil price, and the sometimes related world oil demand, have a heavy influence of rig utilisation.

Political control

Historically, a large number of rigs were deployed in the United States, up to 79% of the active rig fleet back in the early 80s, and around 45% in the last decade. The United States and Canada. Through the liberal nature of the oil business, USA and Canada both react fast to changes in oil price. The rest of the world may react slower, or counter cyclical even; more so in countries where the oil business is controlled by state owned NOCs, and the political influence is higher than economics.

Throughout the latest collapse in oil prices, rig utilisation in different regions changed in very different manner. The effect of the recession seems to be delayed in emerging oil and gas producing countries.

Before, during and after the recession

While North America activity dived at the end of 2014 and emerges from the recession and oil price slump in 2016, countries in Africa were relatively active during the oil slump and seem to feel the effect of the downturn only in 2016-2017. Drilling in the Middle-East went relatively steady throughout the downturn (it’s mostly the production that is manipulated by OPEC, not necessarily drilling). Mexico’s rig utilisation decreased steadily (maybe waiting for the effect of it’s business overhaul), while Argentina held course (mostly targeting long term unconventional gas).

Europe

Beside Norway and UK, both with significant activity offshore North Sea, Turkey has strong drilling activity, sustained by an open market approach.

Africa

Algeria remains a powerhouse in Africa; Libya’s activity is impeded by civil unrest; drilling in many countries in Africa’s South stopped in 2015-2016.

Latin America

Columbia, Ecuador, Mexico are directly impacted by the downturn. Argentina’s drive for unconventional gas goes strong, while in state-controlled Venezuela there are more rigs drilling. The Guyana shelf emerges.

Middle-East

Rig activity in Syria and Yemen collapsed due to wars, as it did in Kurdistan, reflected here in Iraq’s numbers, while Saudi Arabia and Oman increased drilling activity.

Asia-Australia

India is the most active driller, going steady with 28-30 rigs. China, Indonesia and Thailand have strong NOC driven activity. Australia, with an open market, has drilling going up and down with the price of oil.